N: Hello everyone, Welcome to the Less Insurance Dependence Podcast. The official podcast of the reducing insurance dependence academy. www.rid.academy – this is Naren, your co-host. Today’s topic is – can I raise my fees on PPO plans. Can I raise my fees on PPO plans? Before we get into today’s topic, I have a quick announcement to make. We are looking forward to the very first thriving dentist 3 part MBA workshop; this will be happening in the month of 29th of March, 30th of March, and 31st of March as you all know the famous MBA that Garry has been offering for the last couple of years is called 10 elements of a thriving practice. 10 elements of a thriving practice, just like the title suggests, Garry will talk about each one of those 10 elements, and one of those elements is the 24 systems that are at the foundation of every thriving practice that Garry has helped to create over the last 40 plus years. So you are going to learn a ton. It is run in a workshop format, 3 evenings 9 hours of CE, very affordable for less than 200 dollars – go to thrivingdentist.com/MBA, and you can sign up. We run it like a workshop, so the seats are limited, so if there are seats still available, please rush, go to thriving detnsit.com/MBA, and sign up.

You know Naren, as a comment about the MBA, it is a live stream, which means that it is done virtually, but it is done live; this is not recorded – I do these live, and we have lots of engagement with our participants, and we make it a lot more like a workshop, and the cool thing about a live stream is all of our attendees, can be in the comfort of their home or office with no travel, inconvenience and you know to get 9 hours of CE that is for many states that represents a big block of CE towards your license renewal requirements and it is probably the least expensive CE you will ever get. But I did want to make sure that it is done live, as opposed to recorded, and we do that intentionally so we can create more engagement by our workshop attendees. And today’s topic Garry is something that is very interesting, and you and I have been talking a lot, and you have been educating me about, you know, insurance companies and the games they play. I guess one of the famous games they play is they don’t tell people what the maximum fee schedule they will approve is. In fact, I challenge every one of our listeners to call – let’s just pick one; how about Delta. Call Delta and say can you tell me exactly how much I can charge under your PPO plan? First of all, you will likely be laughed off the phone. They are going to say no, no, no doctor, that is not how we do that, you submit your fee schedule, and then we will let you know but then it is kind of like this murky dark sneaky approach. There is nothing transparent about it.

Right

Because they hope that your fees schedule that you submit is lower than their allowed fees because they won’t tell you – no, no, you can actually charge higher for your crown, we will pay up to this. But they will tell you if you are too high, so it is an interesting thing.

So they will never tell you if you are too low, and they will never tell you what that max is so you are like – so lots of doctors that is why they don’t raise their fees because they just don’t want to be rejected or just forget it –

Can you imagine Naren if you owned a restaurant and you decided to serve? Yeah, you are the owner, but you decided to bring out this beautiful meal, and you tell your guest, hey what would you give me for this surf and turf – you got a fillet and a lobster and the patron the diner will say – well wait a minute what do you mean what I will give you for it? How much is it? Well, how much will you give me for it and let’s say the restaurant owner thought you know I would really like to get about 40 dollars for this surf and turf, wait a minute, let me adjust the fees now because that is ridiculous in 2022. If it was surf and turf, it would be more like 80 dollars today, right with the supply chain and inflation that we have.

Yes

So what if the restaurant wanted to get 80 dollars for surf and turf and the patron is playing along, and he says, what – well you know that is a really good looking meal I will give you a 120 for it, and then the restaurant owner says great here you go – you are willing to pay for it but if you came back and said I think that is a 50 dollar surf and turf – the restaurant is going to say no keep going raise it up. That is kind of a murky game that the insurance companies go on.

Yeah – it is a woeful topic, and so technically, the insurance company is not really – I know we have heard people ask the question, you know can I negotiate my- what percentage I get or the fees I get, so I misunderstood. I thought the insurance companies change their policies, and you know sometimes they might not know! do it, and you said that had not been done, and you are correct. What they are doing is they are not really changing how much they are going to pay you. They are just letting you discover through a really complicated process the most you can charge.

Yeah, and it is a one-sided you know system in their favor, and so to answer the question – the title of today’s episode, can I raise my fees on PPO plans? The answer to that is it depends. It is possible, though, and it is possible that the current fees you have with the PPO plan are below the maximum allowable. That is the best way to explain that it is entirely possible – they won’t be above the maximum allowable because your fees schedule would not be approved, but it is entirely possible that it is below, and here is one of the ways that this creeps over time Naren lets say you have been a PPO member for many years, and you don’t raise your fees every year to the PPO plan because you think it is futile but in fact may be inside the PPO plan they have certain cola-type adjustments cost living adjustment and maybe internally- they know that hey we will allow a dentist to raise their fees this minor percent every year, but we are not going to tell them if they don’t do it and it will leave more money on our table and if they do it if they do it and then so be it, but very few dentists will know what the maximal allowable is. So the answer to the question is can I raise my fees on PPO plans is? It depends! If your fees are below the maximum allowable for every service and now let’s complicate it further, Naren, because it is not a handful of fees we are talking about here.

Yeah

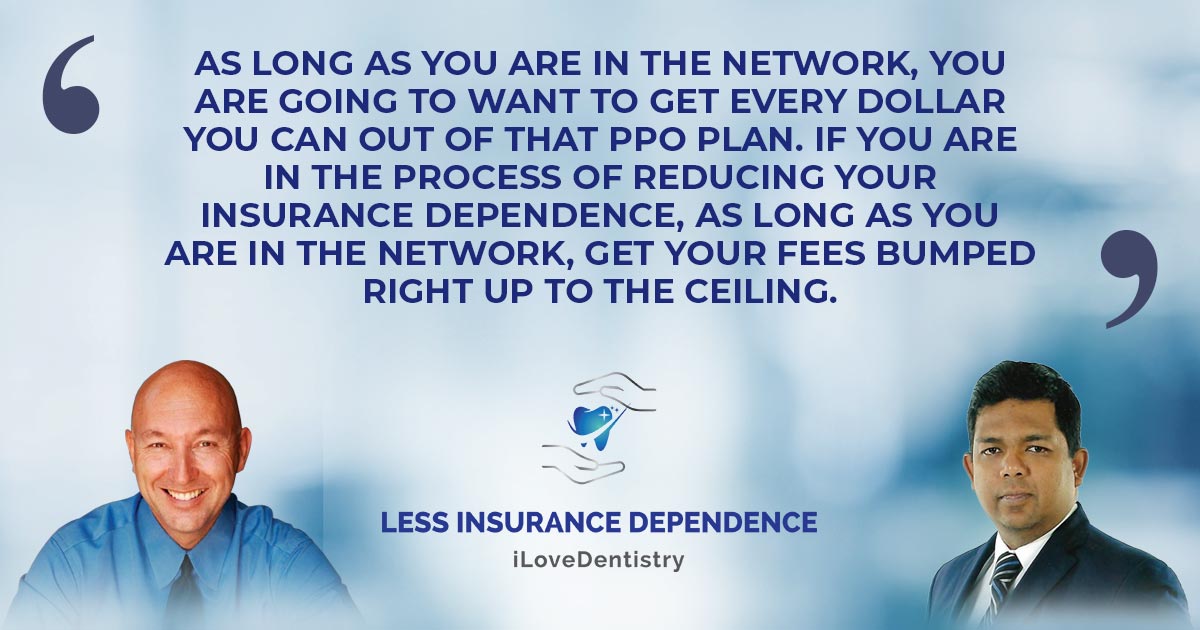

It could be hundreds of fees in a general practice that has a wide range of services. It could be hundreds of fees, so let’s make this actionable, Naren; how are any of our listeners to know if their fees are below the maximum level. Well, I was kidding when I said call the insurance company and ask them because they will not tell you! If you want to verify that, then try it, but they are going to say that is not how it works, doc, and it is a very obscure process. However, there are resources that can help you with this, and Naren, you and I have a colleague – who actually is a very good friend of mine, his name is Ben Taney, and Ben started a company many years ago called Veritas. Veritas – and they can share with you because they work with clients all over the country they know what the maximum allowable is with all the different plans with all the different states they can look at your fees schedule and advise you where to raise your fees – so that you are right at the maximal allowable for each PPO plan, and as long as you are in-network you are going to want to get every dollar you can get out of that PPO plan, and for many of our listeners you are in the process of reducing your insurance dependence, and so as long as you are in-network you are going to want to get your fees bumped right up – right up to that ceiling.

Yeah

Right down to the decimal point! (Laughs) and Veritas can help you with that. We are going to put a recourse we are going to put a website in the show nets for this episode if you are listening, it is Veritas dental resources – VERITAS, dental resources we will put it I the show notes – I would encourage you as long as you are in-network to work with Veritas to get your fees right up to the maximal allowable. Now Ben himself will tell you that that will take you so far, and it could be an improvement over where you are now, but Ben would say ultimately you are going to want to work with Garry to get out of these plans because there is still going not be a big gap between your UCR fees and the maximal allowable, but we are closing that gap a little bit. Does that make sense, Naren?

It makes total sense – so what you are saying is if they are, I am just throwing out numbers here. But if your write off is 45 to 50 percent now, maybe that will come down 5 points, which is still money on your table, which is good, but it is more money and more net profit because your expenses don’t go up a nickel when you raise your fees, it is more net profit in your pocket. But if you think about it – think about you know, imagine this is a bar graph.

Let me throw a curveball, Garry – there are 6 PPO plans that I am signed up with – everyone has to approve my fees, so just because one approved it – the other one does not, then what happens.

Well, that is where you need a resource like Ben because they have totally different fee schedules; don’t think for a minute that they are all the same.

O you need to come up with a fee schedule that all the PPO plans you are with-

Individualize customize for each plan because each one is different. So are you saying that I can charge different amounts for dental patients?

Yes

Absolutely – so if you think of a bar graph and at the top of the bar graph is the UCR fees.

Ah huh

The next rung on this bar graph will be the maximum allowable under the PPO plans – and for many of our listeners, there will be a lower rung on the bar graph, which is where your PPO fees are now. So Ben and Veritas can help you close that gap from where your fees are now – to the maximal allowable, but ultimately if you want to get your full fee, then the next step is to successfully reign from the PPO plans.

Makes total sense.

Does that make sense in terms of sequencing Naren? It does – now I understand it, so it is like a step, so this is like a first step, a baby step, a first step, and an easy step, perhaps a good step to consider. It is an easy step, and all of the gains go right to your bottom line.

Right

You know if you are going to increase, even if this can result in a 50, 60, 70,000 dollars a year increasing your net income – that is fantastic! It won’t get you to the finish line of you being able to charge your usual fees, but it will get you closer to it.

Yeah, I mean when we look at the write-offs, many practices are writing off 400,000, 500,000, and this may not save you 400,000.

I have seen – you know, having referred clients to Veritas, I have seen 6 digital gains.

Ok

But you know if really they are leaving 600,000 on the table and they just improved it by a hundred grand now they are only leaving 500 on the table the 500 is still a whole lot of money.

Yes!

But I would not throw the hundred thousand dollar gain out the window.

Yes, at least in the interim, as you are going through the process of reducing insurance dependence.

And it is a good step it is a really good step, and you know it just depends on where you are and Naren in my coaching work, I always ask you know my clients early in the engagement I ask my client I want you to go back to elementary school., and I want you to use the grading scale that your elementary school teacher sued and we are all familiar with that – ABCD or F and I tell the doctor I know this is totally subjective there is nothing objective about what I am about to ask, and I wish I could objectify but this is going to be very subjective. I want you to rate your practice using the elementary school grading system – ABCD and F on the grade you get from being a relationship-driven practice, and yesterday I did this Naren with potential clients, and his answer was Garry I wish I could give you an answer, but I think it is b- c+ and I said tell me more, he said well – my particular practice has, unfortunately, had not a lot of turnover of because of Covid and I have a relatively new team and because of that our team members don’t know our patients, as well as I, would like them to know – I have a good team right now, and I feel like that C+ B- has lots of room for improvement and I have got the right people who can do it, but if you had to ask me right now – I am going to say B- C+ now that is an honest answer! So I think I have to take him at face value because I am not familiar with his practice yet and his practice that C+ B- is going to take longer to do all the preparedness do the 6 steps, you will have got the 6 steps to successfully resign form PPO plans, it is going to take them a little longer to walk through the 6 steps mainly because they have to build the relationship-driven part of their practice. I want it to be at least an A, if not an A-plus, by the time we start resigning. Like I would not be happy if we said, well, we got it to a B. Am I ready now – well, no!

Hmmm

Not yet, but keep going!

Yes

So I was rely excited about this topic today because I know that for many of our listeners if you think of your readiness being on a spectrum with maybe the right side of the spectrum being they are ready now, then the left side of the spectrum being the other side not even close and then the reality is that most of our listeners are going to fall somewhere in between those, perhaps closer to almost ready.

Right!

But another thing they can do, Naren, if we are talking about readiness, is it is very important that you get your marketing house in order before you resign, and the reason for that is you are going to lose some patients. Naren, you are my mathematician; you do the right math for me – the practice has 2000 PPO patients,

Uh-huh

I am giving you fictitious numbers; I am just making it up; the hypothetical practice I am sharing with you has 2000 PPO patients, and I always tell my clients that you are going to lose between 10 and 15 percent of those!

So you are going to lose 200 to 300 patients.

So let’s use the high number of 15 per year we are going to lose how many?

300

300 – so we have to replace those 300, but hypothetically in this office, they also get 40 new patients every month that comes from the PPO plans by being listed on the PPO plans – so in the course of the year, if you get 40 of those a month, how many new patients during that year are going to come from PPO? 40 a month.

If they get 40 a month in the next year, they are going to get 480.

So now we have to replace over the next year not only the 300 that we lose when we go out of network but the 480 that are not going to come when you resign because that spicket just got turned off. Let’s make 485 500 just to make it around. Then you have got to replace 800 patients in the next year, and the best way to do that is mastering digital marketing! And by the way that even though it is a high number like that – it is very realistic to think that you could replace that with a strong digital marketing plan! Coming to you because you are mastering Google!

Yes!

That is what we did! So you know I want our listeners to understand the sequence in this and understand why it is important to master marketing first. If you get in patients and resign before your marketing is in place, then you are behind the curve because, in marketing, you can’t; it is not just where we flip the switch.

Right

I wish it was, but you told me when I started working with EKWA 5 years ago, and I asked you. I said Naren, I am impatient – how long is this going to take, and you said well Garry, I wish I could tell you with a click of our fingers, but it doesn’t work that way – it is going to take a year to get your marketing fully embodied to get our SEO performing where I want it to perform.

Yes

Now I think you must – I probably expressed a sigh or something. We were doing this over zoom or so, and I went, ‘hmmm,’ and you said Garry, well here is the good news you will start to see noticeable results within 3 months.

Yes

And that is exactly what happened – we had noticeable results, and when I say noticeable results let me define it – it meant that we were listed on page one when someone in our community was looking for a dentist more often than we were before – things started moving in the right direction within 3 months but for you to be happy it takes like a year. Well, you have to earn it if you are doing organic, which is all we do in terms of search; you have got to earn it with Google – now you can pay for it, but it is going to be 20 percent as effective as earned.

Yes

So you can pay, or you can by pay per click because I did not want to wait an entire year – so I went ahead and funded because we had the budget for it – I funded a pay per click campaign, and that is how I filled the gap, but you told me yourself you can do it Garry, but it is going to be 1/5th as effective in terms of money you have to spend 5 times as much money to get the same results without getting any after one year so Naren would you be kind enough to put a link in the show notes for this one? On the marketing strategy meeting that any of our listeners can schedule with Lila?

Absolutely, Garry, it is a – Lila would do 6 hours of research. It is a 900 dollar value, and we won’t charge any fees for it – we will put a link so you can book a martin strategy meeting. Lila would study up on all the things that would matter to Google and tell you where you stand; plus, she will show you a 12-month plan if any of those areas are vague so you have an alternative plan that can get you where you want to get to so it is a wonderful use of your time, we will put that link – EKWA.com/msm.

And just as a reminder, Naren, the reason I wanted to own a practice is that I wanted to have a test kit – so we can test things out, and we could share resources and share what worked and what didn’t work. Well, one of the best hinges that have worked for us is having EKWA as my marketing. I am a paying client of EKWA and very happy because I get better results than we have ever got, and I am spending less than we ever have. Jump on my shoulders and follow my lead. Hey, as we put a ribbon on this episode so to answer that question – can I raise my fees on PPO plans – perhaps. Now you know what that is all about – let me come full circle and remind our listeners to come to join us for the thriving dentist MBA live stream workshop at 3 nights, Tuesday, Wednesday, Thursday – 3 hours a night I get 9 hours of CE it is marching 29th 30th and 31st, and you can register at thriving dentist.com/MBA. Hey, on that note, thanks so much for being a listener of the less insurance podcast, Naren and I look forward to connecting with you on the next less insurance dependence podcast.

One of Gary's most significant achievements as a dental practice management coach is transforming his own practice, LifeSmiles, from one that was infected with PPO plans, no effective marketing strategy, and an overhead of 80% to a very successful dental practice that is currently one of the top-performing practices in the US.

One of Gary's most significant achievements as a dental practice management coach is transforming his own practice, LifeSmiles, from one that was infected with PPO plans, no effective marketing strategy, and an overhead of 80% to a very successful dental practice that is currently one of the top-performing practices in the US.

As CEO of Ekwa Marketing, Naren has over a decade of experience working with dental practices and helping them attract the ideal type of patients to their practices. It is his goal to help dentists do more of the type of dentistry they love with the help and support of effective digital marketing.

As CEO of Ekwa Marketing, Naren has over a decade of experience working with dental practices and helping them attract the ideal type of patients to their practices. It is his goal to help dentists do more of the type of dentistry they love with the help and support of effective digital marketing.